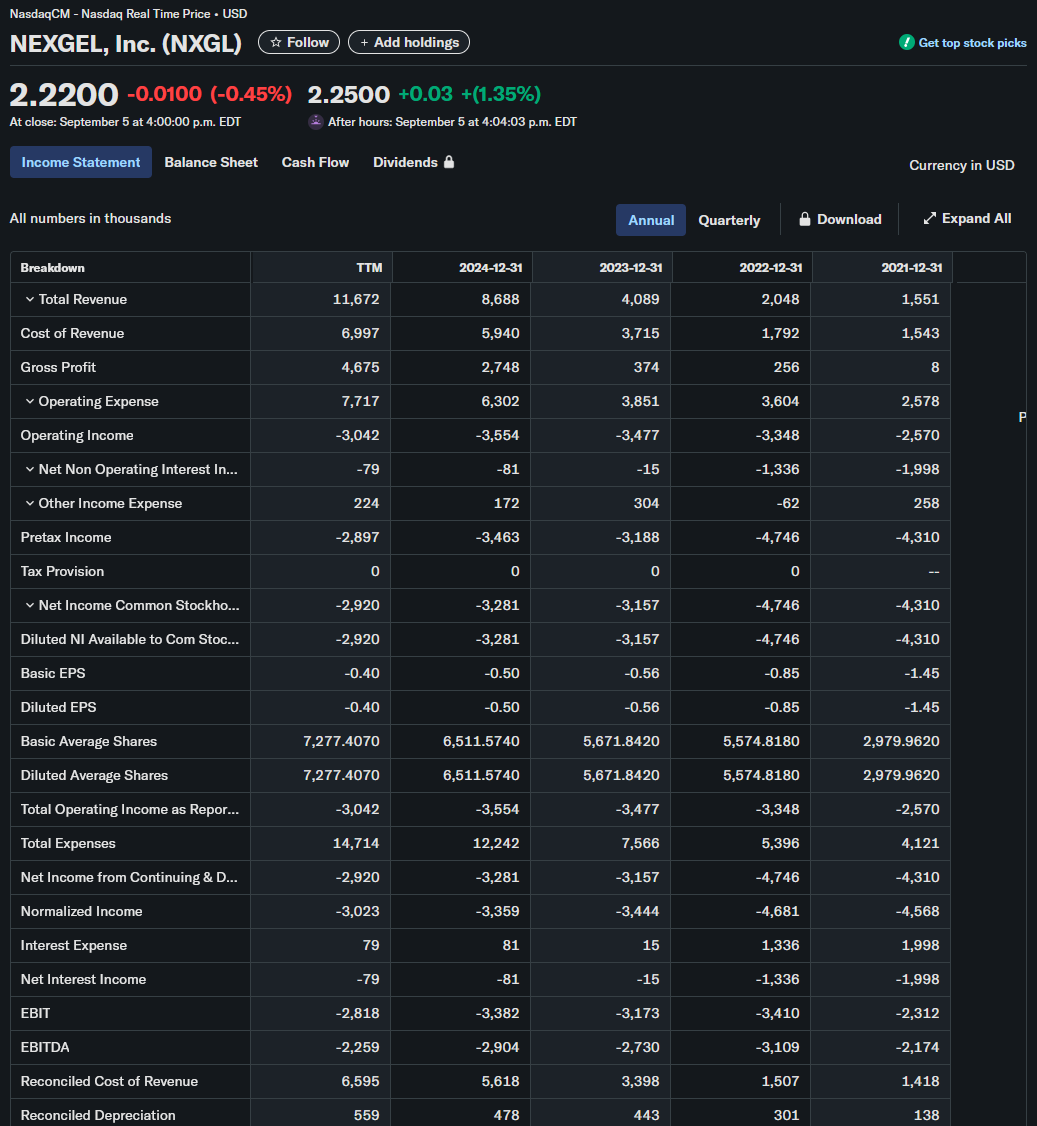

i mean if you look at pic related, it seems like a good risk-reward play, the dilution is expected at this stage but also reasonable, cashburn is decreasing over time so it's a big focus on them, no debt (coz theyre diluting instead lol)

really the risky is they overbuilt their capacity too early i guess? a few years ago they were only at 4% capacity, now they're like ~18% capacity

big reason was that is AbbVie being in talks to get onboarded in 2022 but seeing delays on that on AbbVie's side coz their machiine (which AbbVie acquired for like $550 million) is not completely ready yet