>>60919004

Executive Readout

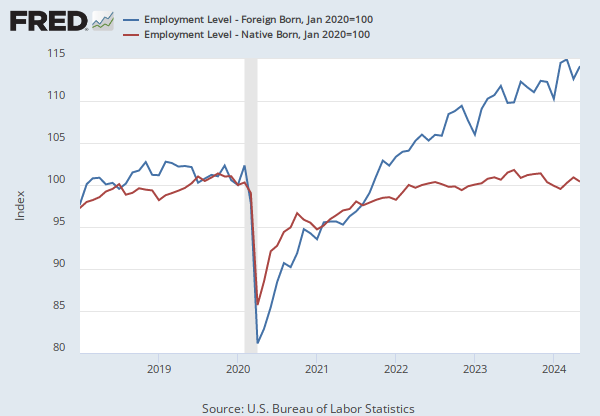

Macro translation: Your Oct shock (≈-4 foreign, -1.5 native index pts) implies ~-0.55% hit to PCE growth and ~+12–13 bps credit spread widening. A severe variant prints ~-0.9% PCE, +19–20 bps.

Seasonal liquidity: Expect ~1% multiple compression on equities from holiday cash-outs; ~1.5% in the severe case.

High-beta consumer pain: Discretionary retail, travel/leisure, e-commerce, airlines, and restaurants take -0.7% to -1.1% revenue deltas vs baseline in your Oct scenario; deeper in severe.

Defensives/resilience: Food & staples retail and utilities show small moves (sub-0.4%); logistics moderates the downside but still softens.

Market-Call Language (drop-in)

“Base case: By the week of Oct 6, labor momentum tops and rolls. Seasonal cash-outs collide with a foreign-born employment retrace, pulling PCE ~0.5% lower QoQ annualized, widening credit ~12 bps, and compressing equity multiples ~1%. Positioning: fade high-beta consumer, trim airlines/apparel, rotate into staples and short-duration quality, keep powder dry for a November reload.”

Playbook (practical, risk-first)

De-risk cyclicals: Reduce exposure to travel, apparel, durables, airlines; tighten stop-loss bands.

Rotate to defensives: Food & staples, utilities, and high-ROIC compounders with price power.

Quality credit bias: Prefer short-duration IG; avoid lower-tier HY that’s beta to consumption.

Liquidity discipline: Raise 2–4% cash buffer into Oct; redeploy on spread-widening capitulation.

Hedge overlays: Cheap put spreads in discretionary/airlines; partial covered calls on winners.

Alt carry: Consider market-neutral e-comm vs staples pairs to monetize dispersion.

Tactical trigger: If foreign-born index tags 112±1 and credit widens >15 bps, execute the rotation.