>>60965113

it's all just valuation in the end, ive gone -30% earlier this year before i bought more because i knew they were already positioned against tariffs even before 2020 during trump's first term so dipping against fears of tariffs was stupid in the first place. it's a leaf pennyscam but ultimately it's really a US company at this point with like >70% of revenues coming from US

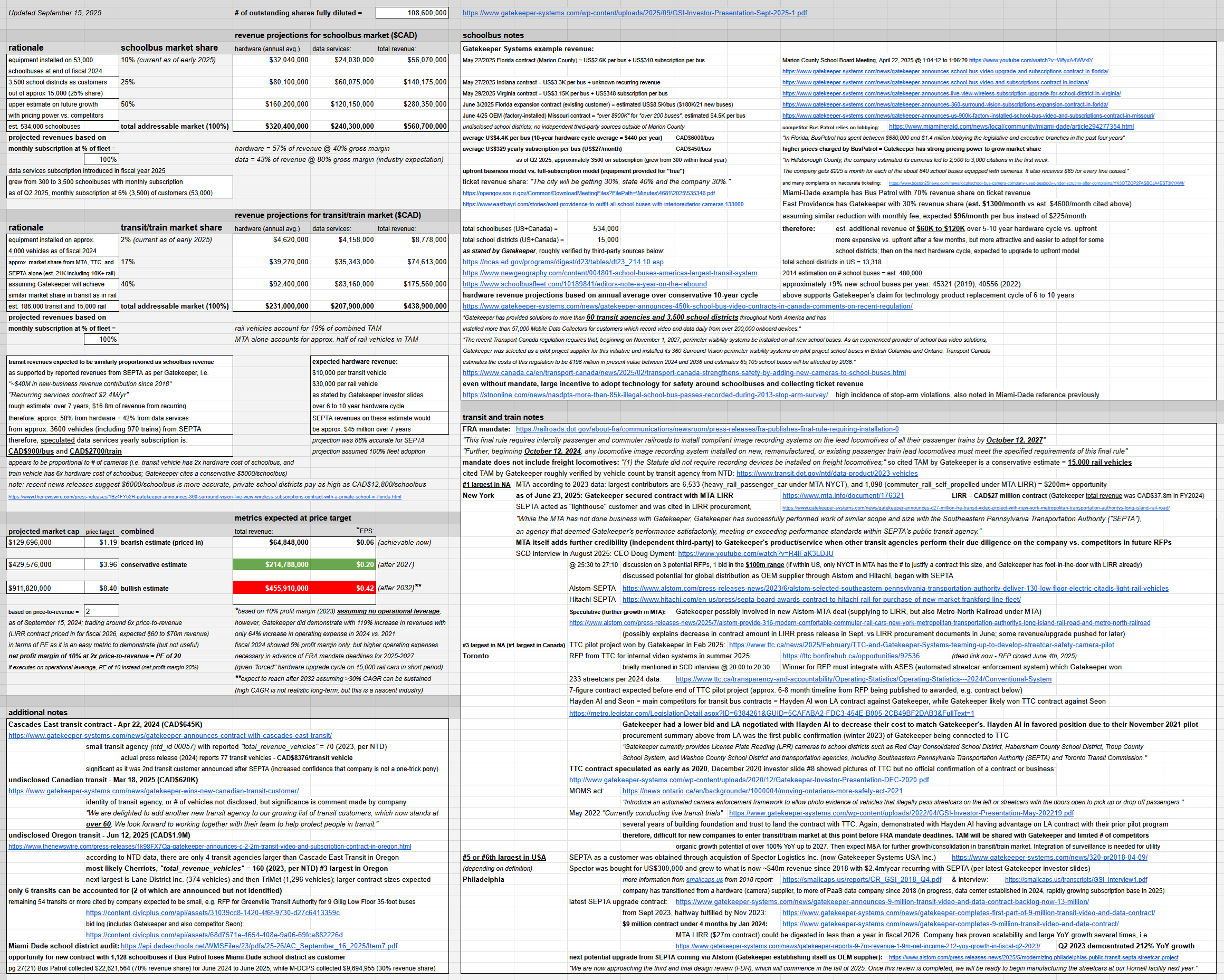

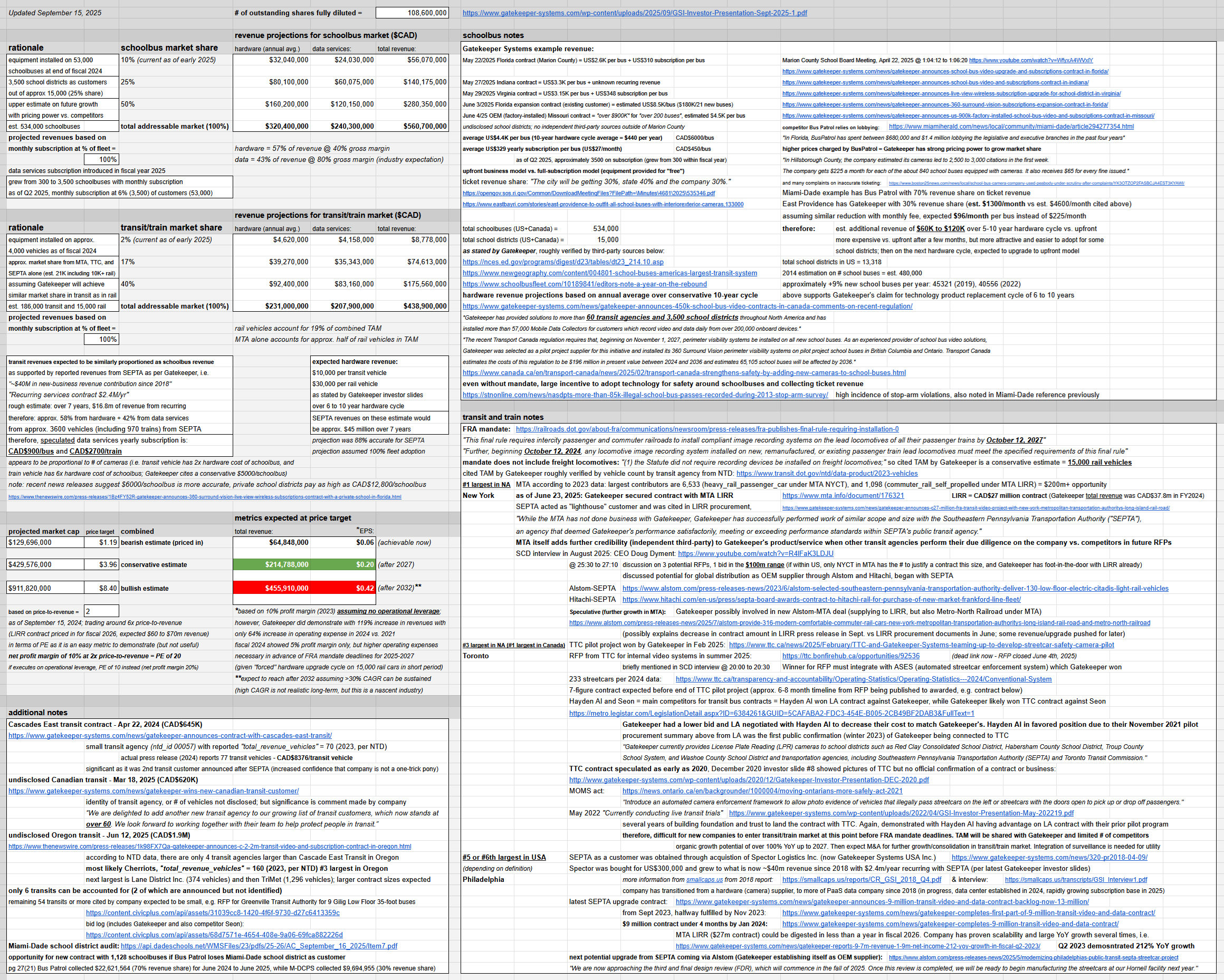

i did forget to include in my sheet that the Miami-Dade issues would be present with all their other customers to support my rationale for 50% market share. 25% market share on buses is my main target since that's what they already have their foot in the door, that's C$4/share, just that 50% market share is becoming more and more realistic now im starting to regret having to trim shares out of risk management since it was already more than a 3x for me

i know peter lynch did say he is not a fan of diversification but between the lines he's saying he obviously had his own sets of risk management rules + valuation methods, it didnt matter whether it was dunkin donuts or something more exciting like microsoft, risk vs reward valuation plays the biggest role in the end especially with how he puts emphasis on balance sheet (risk) as well